A Milestone on the Long Lock-In Recovery Journey: Mortgages Above 6% Exceed Share Below 3%

By Hannah Jones Jan 14, 2026

Mortgage rates have eased from recent highs, but remain above 6%. Rates reached a 2025 peak of 7.04% in January and fell to the 6.2% range by the end of the year. Zooming out, rates have remained above 6% since September 2022, keeping many would-be sellers “locked in” and hindering total inventory recovery. The relatively high share of households with ultralow mortgage rates means that the typical homeowner would see their monthly mortgage payment increase by nearly $1,000 should they choose to sell and buy a median-priced home in today’s high-price, high-rate market.

Housing supply has improved over the past year, tipping the national market into “balanced” territory, and some local markets all the way into “buyer’s market” territory. Scarce inventory has kept upward pressure on home prices, especially in affordable areas where homes continue to sell at a quick clip and buyers face considerable competition. New-construction inventory has helped fill the gap, and the new-home share of inventory has climbed beyond pre-pandemic levels.

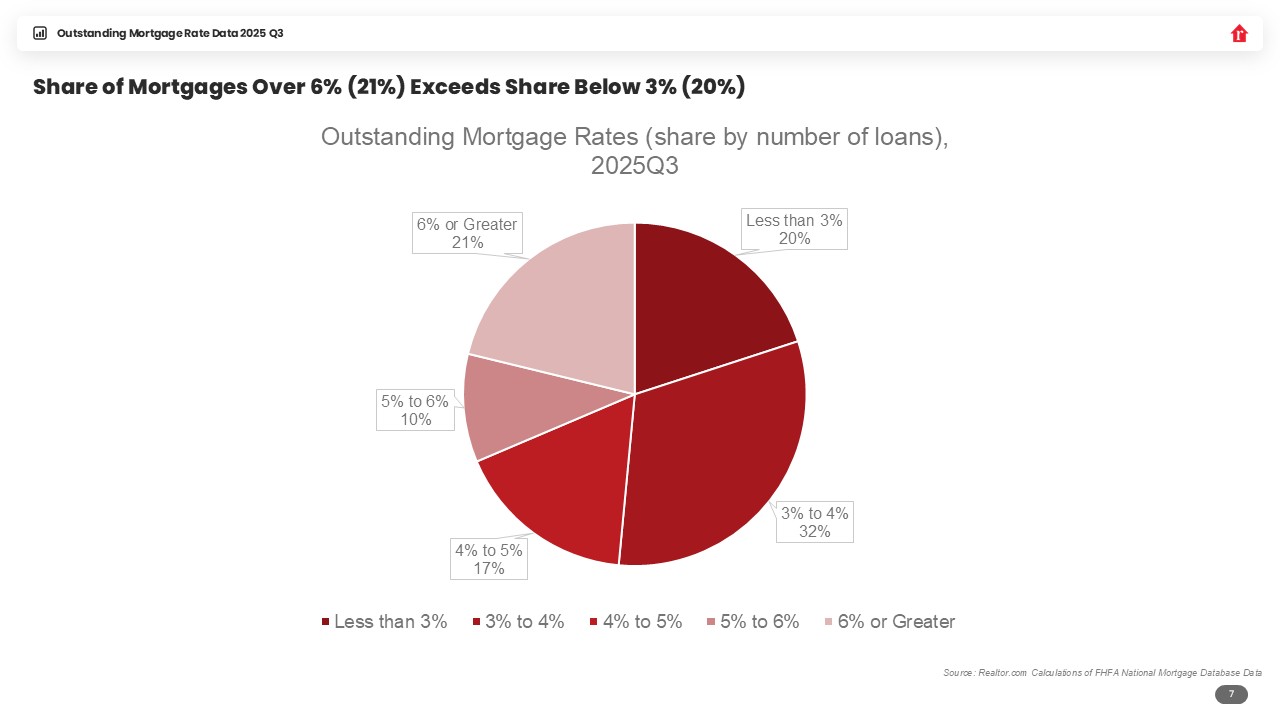

In the third quarter of 2025, 20% of outstanding mortgages had an interest rate below 3%. The Freddie Mac fixed rate on a 30-year loan dipped below 3% in July 2020, and generally stayed below the 3% threshold through September 2021. Highlighting how extraordinary these conditions were, this was the only period in the data’s history (since 1971) where rates dropped below this threshold.

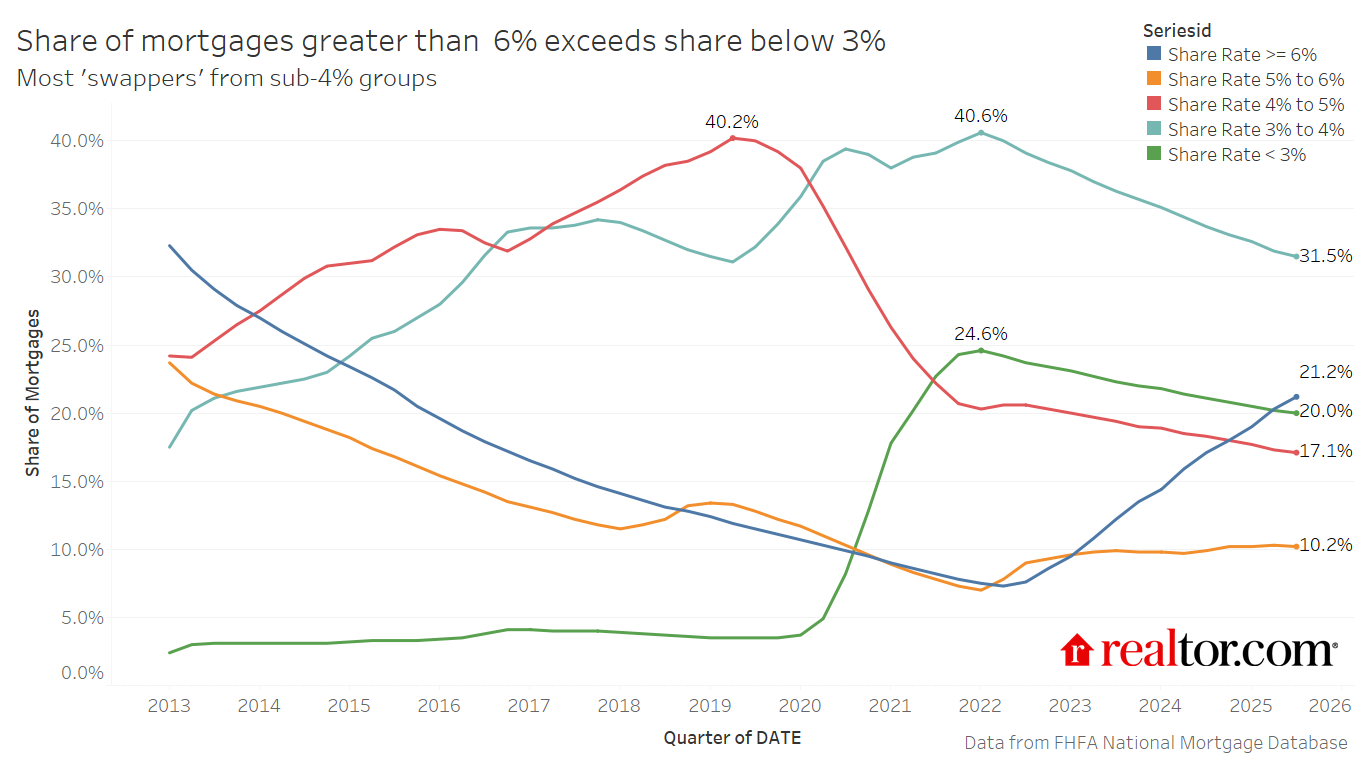

Between the second and third quarters, nearly all of the shifts in share occurred within the sub-4% brackets. This may reflect “swappers,” or borrowers exchanging a lower-rate mortgage for a higher-rate one. The shrinking share of low-rate mortgages could also reflect buyers paying off their mortgages and owning outright. In Q3, the total number of mortgage loans fell both quarter over quarter and year over year, indicating that some mortgages were paid off, not swapped.

At the same time, we’ve observed more builders offering rate buydowns and other incentives, which could be boosting the number of mortgages in the 4% to 6% range and helping to keep those shares stable. Overall, these dynamics resulted in a 0.9-percentage-point increase in the share of mortgages with rates above 6% from the second to the third quarter.

| Outstanding Mortgage Rate | Share of Mortgages (2025 Q3) | Cumulative Share |

| < 3% | 20.0% | 20.0% |

| 3% to 4% | 31.5% | 51.5% |

| 4% to 5% | 17.1% | 68.6% |

| 5% to 6% | 10.2% | 78.8% |

| 6% + | 21.2% | 100% |

Source: FHFA National Mortgage Database

Nearly one-third of outstanding mortgages (31.5%) carry interest rates between 3% and 4%. Meanwhile, 17.1% fall in the 4%–5% range, 10.2% are between 5% and 6%, and 21.2% have rates of 6% or higher.

The increase in mortgages with rates above 5% likely reflects several dynamics. Some households that had delayed moving in anticipation of lower rates may have decided to act as mortgage rates softened, making the timing feel more favorable despite still-elevated borrowing costs. Additionally, with the typical rate in the low-6% range, some buyers were likely able to lock in or refinance below 6%, boosting the 5%–6% share.

Altogether, this means that more than half (51.5%) of outstanding mortgages still have a rate of 4% or lower, and roughly 69% have a rate of 5% or lower. Looking at the year ahead, we expect that the Q4 2025 data could show the share of mortgages below 6% falling close to 75%. Put differently, we expect the share of mortgage holders with a rate of 6% or higher to increase as home shoppers purchase a home in the current 6%-plus rate environment. Recent mortgage rate progress into the low end of the 6% range could encourage some homebuying activity.

The share of homeowners holding a mortgage with a rate of 6% or higher increased more than 4 percentage points between the third quarter of 2024 and the third quarter of 2025 as buyer activity carried on despite high rates. Even in today’s high-price, high-rate market, homebuying activity around big-life events (e.g., kids, marriage, divorce, etc.) keeps the market in motion. Though the lock-in effect continues to affect the market, a recent survey revealed that 40% of potential buyers would find a home purchase feasible if mortgage rates were to drop below 6%, and 32% of buyers would be willing to participate if rates dropped below 5%. Easing inflation and mortgage rates will be key drivers of seller activity, which will relieve some of the price pressure and competition in today’s undersupplied market.

Notably, the share of mortgages with rates above 6% now exceeds the share with rates below 3%. While roughly 80% of outstanding mortgages still carry rates below 6%, indicating that rate lock-in remains substantial, this shift marks a meaningful inflection point, suggesting increased market movement as more households either trade in low-rate mortgages for higher-rate loans or enter the market for the first time.